Trust But Verify

no one does it better.”

Dr. Joseph T. Wells, CFE, CPA

Association of Certified Fraud Examiners

One Honest Soul

In 1999 Tom led his Chicago Forensic Accounting team to a Latin American country (Guatemala for purposes of Tom’s second novel ONE HONEST SOUL) to confront a monster. The plant GM preyed on his workers treating them in the most horrible of ways. If not for one of those employees coming forward, Tom doubts he would have been able to solve this fraud which was the largest fraud discovery of Tom’s entire career. So large, SEC Regulations required it be disclosed in the company’s 10K filing. While Tom’s novels are fiction they are all inspired by real investigations.

Sunday Nigh Fears

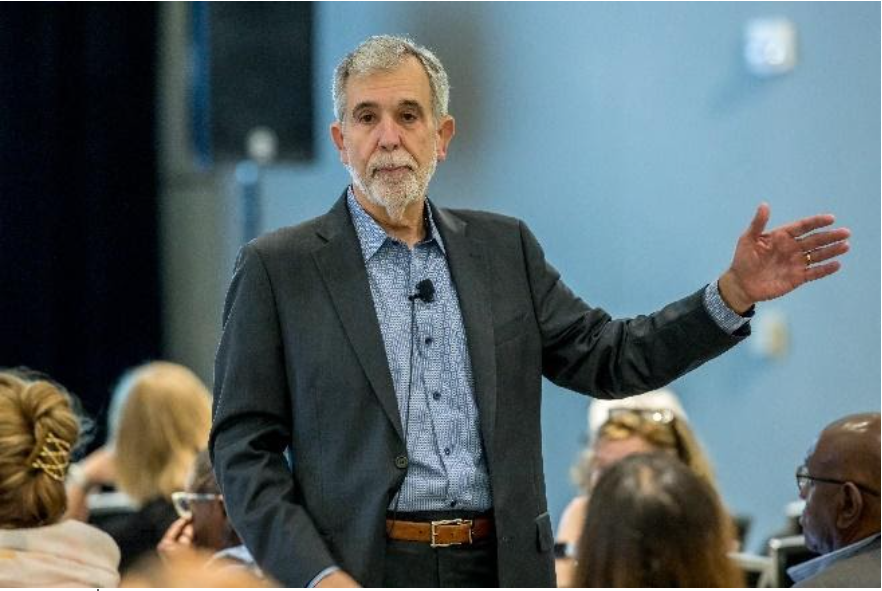

Tom tells an audience of financial statement auditors how he discovered a massive leasing scam on his first public company audit. It would become the inspiration for his first novel SUNDAY NIGHT FEARS. He has given similar speeches around the country warning auditors how such hidden frauds could survive detection on annual audits. Auditors are not trained in the art of fraud investigation, nor is it their responsibility to find fraud.

Encourage Others to Talk

While Tom spent most of his career investigating financial crimes across the globe, he first had to sell himself to prosecutors, attorneys, and audit committees in order to be engaged. In 2019 he developed a 75-minute seminar explaining his winning selling techniques. This is a short snippet of one of them—Encourage Others to Talk About Themselves.

WHAT AUDIANCES SAY ABOUT TOM:

- “Bring him back! Outstanding delivery in a fun and lively manner.”—Brett

- “I thoroughly enjoyed his manner, stores and his insights.”—Bethany

- “Thank you for booking the best speaker that I have ever heard and witnessed in my 17-year professional career. I thought Tom Golden was a phenomenal speaker.”—Jonathan

- “Best session at the conference….should have been scheduled for two sessions.”—Katie

- “Tom draws from his vast experience to illustrate key concepts using an interactive presentation style that keeps the audience highly participative in discussions.”—Vairam

- “You did it again! Your presentation was a real bell ringer and has become the gold standard.”—Steve

ACFE Global Fraud Conferences 2018 and 2019 Pulled from seminar audience evaluations:

- “Tom’s message and his straight-forward presentation was outstanding. In addition, his humor and wit made the presentation very entertaining…”

- “My favorite session… Loved his energy and passion! Would love to attend more sessions with Tom in the future! Very inspiring! Wish I could have worked for him early in my career.”

- “This was my absolute favorite session. Not only was the information presented extremely valuable to apply to my work life but also my home life. The presenter was very engaging and funny. He gave so many examples how to apply the information… I would absolutely love to take another class from him in the future!”

- “Tom just keeps getting better with age!”

Speaking Query

Fill out this form to inquire about Tom’s availability